Escalating Port Congestion strains Container Shipping Flows : Drewry

LONDON : Port congestion across key Northern European hubs is intensifying, with Bremerhaven particularly affected by labour shortages during the recent holiday period. Compounding the situation, low water levels on the Rhine are limiting barge capacity, particularly out of Antwerp and Rotterdam—further straining inland logistics.

Major gateways including Antwerp, Rotterdam, Hamburg, and Bremerhaven are now grappling with escalating backlogs, as containerships face mounting delays. At the Port of Antwerp-Bruges, operations were further strained by a nationwide strike on 20 May, which temporarily disrupted vessel traffic. Kallo and Boudewijn Locks were affected, with Boudewijn Lock later restored to full operation by the evening. Although the impact was short-lived, it added pressure to already congested conditions across the region.

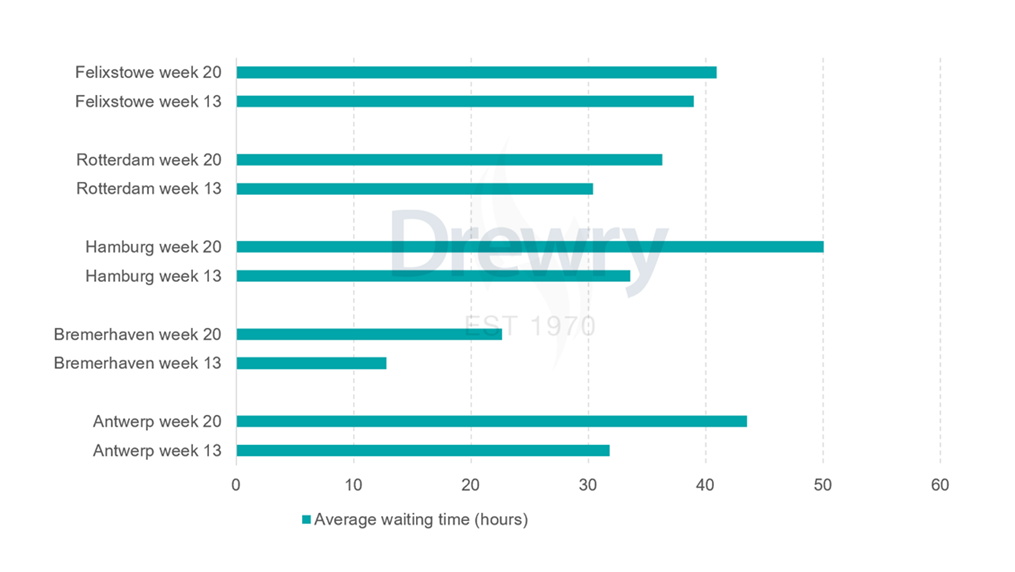

Figure 1: Average containership waiting time – Week 13 vs Week 20 (hours)

As illustrated in the chart above, berth waiting times at Antwerp have risen from 32 hours in Week 13 to 44 hours in Week 20—a 37% increase. Similarly, Hamburg has seen a 49% surge, with waiting times climbing from 34 to 50 hours, while Bremerhaven saw 77% increase, over the same period.

This growing congestion is having a cascading effect across the supply chain:

• Supply chain reliability is deteriorating

• Logistics costs are rising

• Inland transport is becoming increasingly complicated

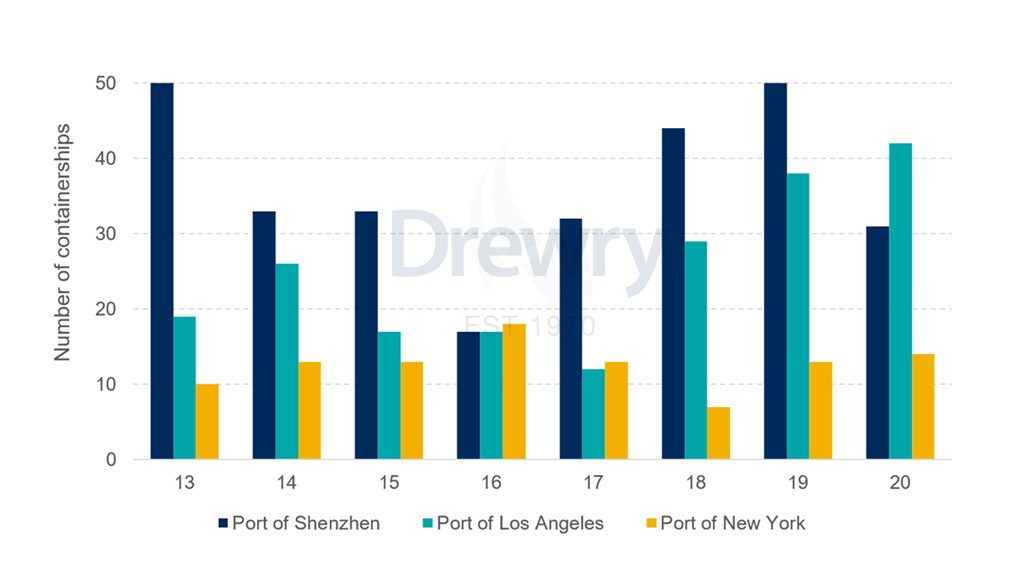

The issue isn’t limited to Europe. Similar patterns are emerging in Shenzhen, Los Angeles, and New York, where the number of containerships awaiting berth has been increasing since Week 17. Peak congestion figures show Shenzhen with up to 50 ships waiting, Los Angeles with 42, and New York with 14, as seen in the chart below.

Figure 2: Number of containerships waiting outside key ports, by week

Port delays are stretching transit times, disrupting inventory planning, and pushing shippers to carry extra stock. Meanwhile, carriers are rerouting vessels and introducing congestion-related surcharges. For example, MSC will introduce a congestion surcharge from 1 June on all cargo moving from Northern Europe to the Far East, adding to rising shipping costs.

Adding to the pressure, the Transpacific eastbound trade is showing signs of an early peak season, fuelled by a 90-day pause in US–China tariffs, set to expire on 14 August.

As a result:

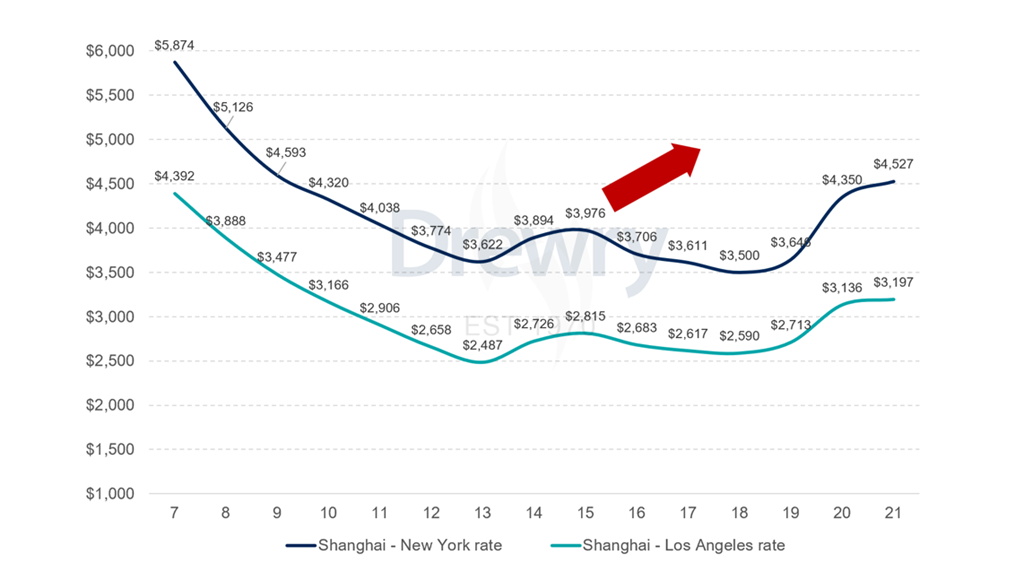

• Container spot rates on transpacific routes have surged 27% since early May, as shown in the chart below tracking the sharp rise in Drewry World Container Index (WCI). Rates from Shanghai to Los Angeles climbed from $2,590 on 1 May to $3,197 by 22 May, while rates to New York jumped from $3,500 to $4,527 over the same period, reflecting intensified demand and successful general rate increases.

• General Rate Increases (GRIs) were successfully implemented on 15 May

• Additional GRIs and Peak Season Surcharges (PSSs) are planned for 1 June

Figure 3: Drewry World Container Index (US$/40ft container), by week

The situation reveals the exposure of container shipping to disruption and underscores the urgent need for resilient, adaptive supply chain strategies.

In such a volatile environment, access to up-to-date market insights, including operational metrics such as port congestion, cancelled sailings, and capacity, is essential in helping cargo owners make informed decisions, mitigate risks, and navigate ongoing uncertainty more effectively.

Source: Drewry