India-EU FTA positions India to capture market share from Bangladesh

NEW DELHI : India–EU Free Trade Agreement (FTA) can give India a significant competitive advantage in apparel exports over rivals like Bangladesh, Vietnam, Turkiye, Pakistan, and China, and India’s cotton-dominant industry is a key strategic asset in this context.

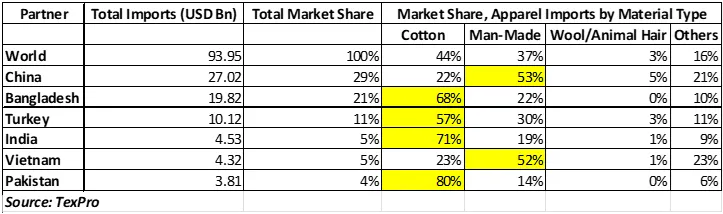

Currently the EU has the following mix in terms of apparel imports:

China and Vietnam have MMF apparels as major share while Bangladesh, India, Turkiye and Pakistan have cotton apparels as major share. Now the cotton share in specific can be tapped by India as summarised below:

- Tariff advantage: Level playing field with competitors

Before the FTA, Indian apparel exporters faced ~9–12 per cent tariffs in the EU on many products. Competitors such as Bangladesh, Pakistan, and Turkiye already had preferential or zero tariff access through existing schemes or agreements, giving them a clear price edge. The FTA eliminates tariffs (zero-duty) on nearly all apparel and textile tariff lines entering the EU. This corrects India’s long-standing tariff disadvantage vis-à-vis Bangladesh, Pakistan, and Turkiye.

- Trade share opportunity: Growing EU market presence

Right now, India’s share of the EU apparel market is relatively low (~4 per cent), while China, Bangladesh, and Turkiye command larger slices. Post this FTA, India’s share could rise to 8–9 per cent or more over the medium term as cost competitiveness improves. European brands are already showing interest in increasing sourcing from India.

- India’s cotton advantage

India’s apparel and textile industry is deeply integrated around cotton: India is one of the world’s largest cotton producers with strong capacity across spinning, yarn, fabric, and garmenting. This vertically integrated cotton ecosystem reduces dependence on external fibre sources and lowers costs for cotton-based products. In contrast, Bangladesh is a garment-centric economy but imports most of its fabric/yarn (often from India). Vietnam and China have strengths in man-made fibre (MMF) and synthetic garments, not just cotton. Pakistan also has cotton production but at a smaller scale and limited integration with large global buyers than India. Thus, cotton strength helps India in categories where Europe demands cotton apparel, home textiles and high-value cotton made-ups, sectors where raw material access and processing capacity matter a lot.

However, for MMF/synthetic heavy segments (where China, Vietnam excel), the advantage is less pronounced unless India scales up in those fibres too.

- Non-tariff and compliance factors

EU buyers increasingly emphasise standards like sustainability, traceability, and rules of origin, which can affect competitiveness. Indian exporters will need to meet EU regulatory and compliance requirements efficiently to fully benefit from the agreement.

- Overall competitive landscape vs major rivals

Overall, India has a big advantage with the India-EU FTA, specifically against countries like Bangladesh, Pakistan, and Turkiye. However, Vietnam and China still hold strong due to MMF dominance in apparel as well as due to China’s scale.

India’s apparel exports to the EU could nearly double from ~$7 billion today to $13–15 billion by 2032 under FTA conditions. India will likely overtake Pakistan and Turkey in key apparel segments and narrow gaps with Bangladesh and Vietnam. China will remain large, but India gains a tariff edge in cotton RMG, strengthening its position for EU buyers.