Asia-US container rates fall as new ships enter market at record pace, scrapping wanes

LONDON: Rates for shipping containers from east Asia and China to the US fell this week, and analysts at supply chain advisors Drewry said increased deliveries of new ships and a slowing scrapping program are one of the reasons.

“Deliveries of new containerships averaged 180,000 TEU (20-foot equivalent unit)/month in 2025, while demolitions reached only 6,000 TEU/month over the entire year,” Drewry said in a market opinion published this week. “More new orders will only continue to fuel this imbalance and create a deeper hole for carriers to climb out of.”

Drewry said in response to this weak demand ahead of factory closures, carriers have aggressively managed capacity by announcing 18, 27 and 28 blank sailings over the next three weeks, a frequency much higher than in previous years.

But some analysts think the surge in newbuilds is too much to overcome through blank sailings.

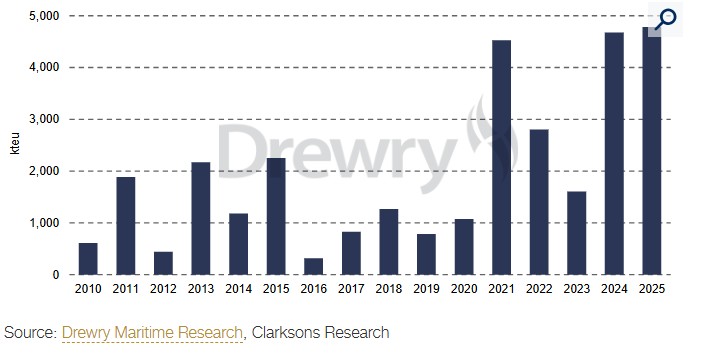

The following chart shows the sharp increase in orders for new vessels, which began in 2021, and has seen the largest number of orders since at least 2010 in the past two years.

Lars Jensen, president of consultant Vespucci Maritime, said the container shipping orderbook relative to the size of the fleet in operation is now above 34%, which is very high.

“We have not seen the orderbook ratio of this magnitude on this side of the financial crisis a decade-and-a-half ago,” Jensen said.

The share of vessels older than 20 years is now at 17%, Jensen said, which means a significant portion of this might well be scrapped as overcapacity hits the market in the coming years.

“But not all of them, as this would lead to potential bottleneck issues related to smaller container vessels,” Jensen said. “But even with a high level of scrapping, it is presently difficult to see how demand can fully keep pace with the new vessel injections.”

CONTAINER RATES

Rates were lower to both coasts from all analysts tracked by ICIS.

Rates from global logistics company Freight Right on its TrueFreight Index (TFX) fell for the third week in a row, as shown in the following chart.

Robert Khachatryan, founder and CEO of Freight Right Logistics, said the ocean freight market has entered a phase of significant decline as the industry moves through the Lunar New Year period.

“Rates have retreated further than market analysts initially projected, reaching levels that challenge carrier profitability,” Khachatryan said.

Rates from Drewry fell by 8% to the US West Coast and by 5% to the East Coast, as shown in the following chart.

“This downwards trend highlights a significant shift in the market, as the traditional pre-Lunar New Year cargo rush – which typically bolsters demand – is failing to materialize in 2026,” Drewry said.

Rates from online freight shipping marketplace and platform provider Freightos edged lower this week.

Judah Levine, head of research at Freightos, also attributed some of the decline to more newbuilds entering the market.

“Prices across these lanes are significantly lower than this time last year due partly to fleet growth,” Levine said. “[Global container shipping line] ONE identified overcapacity as one driver of Q3 losses last year, with lower volumes due to trade war frontloading the other culprit.”

Container ships and costs for shipping containers are relevant to the chemical industry because while most chemicals are liquids and are shipped in tankers, container ships transport polymers, such as polyethylene (PE) and polypropylene (PP), which are shipped in pellets.

They also transport liquid chemicals in isotanks.

LIQUID TANKER RATES

US chemical tanker freight rates as assessed by ICIS were largely unchanged this week with contract of affreightment (COA) nominations steady for most trade lanes.

For the cargoes in the South American trade lane, COAs remain strong leaving very little spot availability. A large parcel of ethanol fixed USG to San Luis, and several others were quoted for second half of February, but inquiries remain limited for spot cargoes.

Similarly, for the USG to ARA trade lane, it was another off week with only a few reported fixtures, as the market remains fully supported by steady COA nominations.

However, there were some unusual cargoes fixed for products like caustic soda and ethanol.

Some styrene was reported fixed from Lake Charles to ARA. Overall, rates seem to be maintaining current levels.

There was no difference along the USG to Asia routes, as it was another quiet week on this trade lane.

Spot rates remain steady as the 1H February space across the regular carriers is sold out.

Some of the larger players should have space in the second half of February depending on COA nominations. The chemical COAs have been steady through 1H March, but still in the tentative phase.

Several inquiries were seen for methanol, ethanol, vinyl acetate monomer (VAM), styrene, and MEG.

On the other hand, bunker prices were unchanged this week but overall remain strong.

Source: ICIS