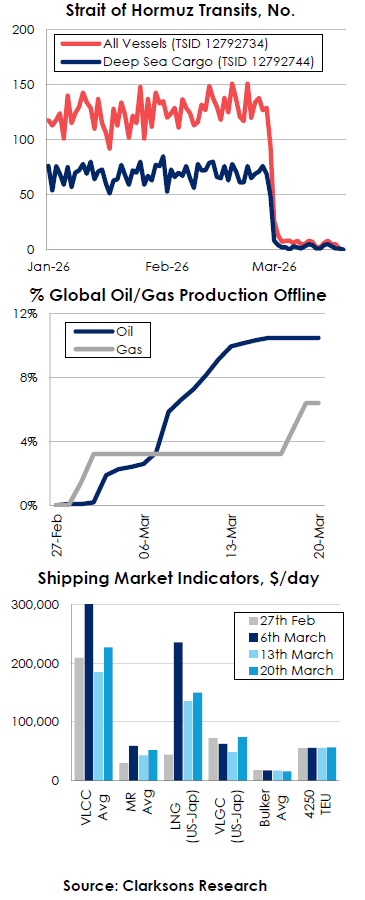

Middle East Conflict: Straits of Hormuz Transits Remain 95% Down

LONDON: Clarksons Research, the data and analytics arm of the Clarksons Group have been closely monitoring shipping activity and markets impacted by the conflict.

Summarising their latest update issued today at 12.00 am 23rd March, Steve Gordon, Global Head of Clarksons Research commented :

- Strait of Hormuz transits still remain 95% down on pre-conflict levels (avg. 4 transits per day past week vs ~125 pre-conflict) with 75% of transits have been exiting the Gulf in the past week

- ~10 oil tankers (12m bbl) estimated to have transited through the Strait over the past 7 days (versus 250 vessels of 300m bbl in a normal week)

- ‘Trickle’ of very large LPG carrier transits continues, with 2 recorded yesterday and 2 Indian-linked vessels passing through the Strait today (~80% below normal over the past week)

- Crude exports from Yanbu are now running at ~4m bpd (up from 1m bpd, potentially increasing to 5m bpd, and with ~40 VLCCs waiting/enroute), while arbitrage dynamics supporting long-haul US oil and gas exports

- 10% / 6% of global oil / gas supply offline, alongside 3% of global refining capacity

- Excluding locally trading vessels, there are ~1,100 ships (37m GT of $30bn) currently inside the Gulf. This total includes ~300 oil tankers, including 6% of crude tanker (8% of VLCCs) and 4% of product tanker tonnage as well as 4% of VLGC and 1% of containership and bulker tonnage

- Vessel charter rates across tanker and gas remain elevated despite loss of cargo volume, with a range of ‘mitigating’ factors currently lending support

- Energy shipping markets for now remain at elevated levels (VLCC earnings at $227,000/day, MRs $52,000/day, LNG firmer w-o-w, rising to $150,000/day, VLGCs up to $74,000/day). Bulkcarrier earnings are steady for now ($15,000/day), while container freight rates have edged higher (knock-on logistical disruption has so far been more limited than initial expectations and rates remain well below Covid-19 levels)

- The cost of moving a barrel of crude oil remains elevated at $10/bbl (on a US Gulf – Asia voyage), up from $5/bbl at the start of the year.

- High bunker prices (e.g. VLSFO in Singapore stands at ~$1,000/t, >100% vs start-26) amid oil supply shortages – our data suggests that average container vessel speeds are down 2% across March so far.

- Prior to the conflict, 20% of global oil supply passed through the Strait of Hormuz, including 37% / 19% of seaborne crude oil and products trade. 19% of global LNG trade (3% of global natural gas supply) also passed through the Strait, alongside 28% of global LPG volumes (~10% of supply), as well as 13% of seaborne chemicals, 9% of cars, 4% of dry bulk and 3% of container trade volumes

See below graphs (underling data available on request).

About Clarksons Research

Clarksons Research, the data and analytics arm of Clarksons, is the market leader in the provision of independent data and intelligence across shipping, trade, offshore, and the maritime energy transition. Millions of data points are processed and analysed each day to deliver trusted insights to thousands of stakeholders across the maritime sector. Better data for better decisions.