Reefer container freight rates to outgun dry cargo rates in 2022

LONDON : Reefer container freight rates have risen sharply through 2021, but in contrast to dry cargo rates, are forecast to rise further in 2022, driven by catch up on North-South routes, according to Drewry’s recently published Reefer Shipping Annual Review and Forecast 2021/22 report.

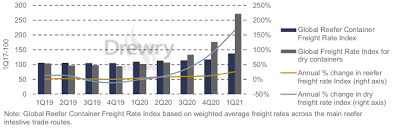

Drewry’s Global Reefer Container Freight Rate Index, a weighted average of rates across the top 15 reefer intensive deepsea trade routes, rose 32% over the year to 2Q21 and by the end of 3Q21 these gains are expected to reach as much as 50% (see chart). But these advances are dwarfed by the recent surge in dry container freight rates which have seen average container carrier unit revenues more than double over the same period.

The resurgence in reefer freight rates has not been uniform across all trades. Pricing recovery has been particularly strong on the main East-West routes, where vessel capacity conditions have been noticeably tight. But North-South trades have generally seen less price inflation, particularly on export routes from WCSA, Central America and Southern Africa.

“In contrast to dry container freight rates which are expected to decline in 2022 as trade conditions normalise, reefer container freight rates are forecast to continue rising as price inflation feeds into North-South routes when long term contract rates are renewed,” said Drewry’s head of reefer shipping research Philip Gray. “Most reefer cargo on these trades moves on long term contracts.”

Drewry Global Reefer Container Freight Rate Index

The key driver of reefer freight rate inflation has been capacity related, as perishables shippers have competed with higher paying dry freight BCOs for scarce containership slots, despite ample reefer plug capacity provision. Meanwhile, continued disruption across container supply chains has led to acute shortages of reefer container equipment, already challenged by the particularly imbalanced nature of reefer trades.

“We believe that these conditions are short term and will self-correct as trade normalises from mid-2022,” added Gray. “However, we expect reefer container equipment availability to remain an issue for certain trades during their peak seasons, as the global fleet is not expected to keep pace with rising cargo demand, despite record output of newbuild containers.”

These conditions have provided short term reprieve to specialised reefer vessels, as some BCOs have returned to the mode seeking relief from congested container supply chains. But despite these developments Drewry estimates that the specialised reefer vessel’s share of the perishables trade fell to 12% in 2020 and is expected to decline further into single figures over the next few years.

Hence, despite a 0.4% decline in global seaborne perishables trade in 2020 to 132 million tonnes, containership reefer liftings advanced 0.3% to 5.4 million teu. Further modal share gains and buoyant cargo demand will see containerised reefer traffic expand at a faster pace than dry cargo trade from 2022.

The contraction in overall seaborne perishables trade in 2020 was much milder than for dry cargo, demonstrating the stronger resilience of reefer trades to economic shock. The trade was particularly impacted by a shuttered hospitality sector which reduced demand for deciduous fruit, fresh vegetables and frozen potatoes, while Covid-19 containment measures cut crop production and fish catches. Meanwhile, an outbreak of fusarium TR4 disease in the Philippines weakened growth in banana trades. But cargo demand was supported by a booming pork trade, owing to African Swine Fever driven imports into China.

Seaborne reefer traffic picked up through 1H21, expanding 4.8% YoY, led by meat, citrus and exotics trades but is not expected to expand at the same pace as dry cargo through the remainder of the year as it is not recovering from as deep a contraction in 2020.

“A combination of buoyant cargo growth and tight capacity conditions will continue to support reefer container freight rates and specialised vessel charter earnings,” concluded Gray. “However, charter rates for larger reefer vessels that have been in particularly high demand of late are expected to wane as capacity conditions ease.”

Source : Drewry