Sea-Intelligence reports no consolidation impact on ocean carrier competition

COPENHAGEN : In Issue 675 of the Sea-Intelligence Sunday Spotlight, the Danish shipping data analysis firm examined whether the turmoil of the last four years has led to the largest carriers growing in dominance versus the mid-tiered carriers, or has been an opportunity for mid-sized carriers to gain in importance versus the big carriers.

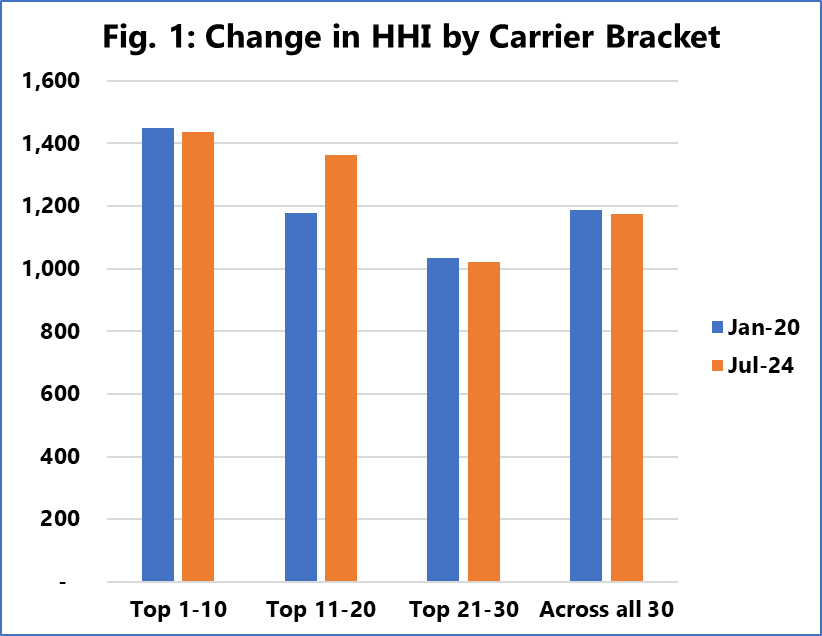

To assess this, Sea-Intelligence calculated the global Herfindahl-Hirschmann Index (HHI) for the top 30 carriers, dividing them into three equal segments. The HHI is a gauge of industry consolidation: an HHI below 1,500 indicates low concentration, 1,500-2,500 suggests moderate concentration, and above 2,500 reflects high concentration.

For the overall industry, represented by all 30 carriers combined, the HHI has decreased slightly, remaining below 1,200 and indicating a low concentration level. The concentration among the top 10 carriers has remained largely stable despite recent disruptions. Similarly, the concentration for the bottom third (ranks 21 to 30) is unchanged.

However, there has been a modest increase in concentration among the carriers ranked 11 to 20, though this level still remains under the 1,500 threshold, comparable to the competitive pressure among the largest carriers.

Overall, the data suggests that despite concerns from shippers about industry concentration, the global concentration remains within the bounds of what is considered normal, with recent market upheavals neither significantly increasing nor decreasing these levels.