Ripple effects of US tariffs and geo-political turmoil continue to spread across ocean container shipping

OSLO : US President Donald Trump threw a rock into the already turbulent waters of ocean container shipping when he announced sweeping US tariffs on China and the rest of the world in April.

If you are a shipper, it is imperative that you understand how these tariffs are still casting ripples across global ocean supply chains in increasingly-subtle and nuanced ways.

The US tariff ripple effect

Ocean container shipping demand from China to the US fell off a cliff in the aftermath of the “Liberation Day” tariffs in early April and carriers responded to falling freight rates by shifting capacity off these trades in favour of trades such as North Europe and South America East Coast.

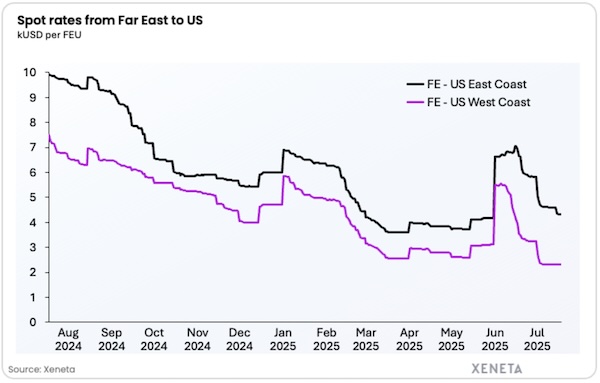

When the US and China agreed to lower tariffs in mid-May, shippers hit the accelerator to take advantage of the 90-day window of opportunity by importing as many goods as possible (or appropriate). This cargo rush saw a spike in average spot rates between 31 May and 1 June of 75% into the US West Coast and 58% into the US East coast.

Carriers responded to the cargo rush by shifting capacity back onto these US trades as quickly as possible. With the pendulum having swung back again, capacity is outweighing demand and average spot rates are plummeting, down 58% into the West Coast and 35% into the East Coast since 30 June.

Ripple effects distort trade relationships

Shifting capacity between trades takes time and is not like flicking a switch.

What is significant in the example above is that carriers prioritized rushing cargo back to the US West Coast trades rather than the US East Coast following the 90-day lowering of tariffs.

A faster return of capacity into the US West Coast means spot rates began to soften sooner than into the US East Coast and this has distorted the delta we would ordinarily expect to see between rates on these US fronthauls.

Average spot rates from Far East into the US West Coast have historically been around USD 1000 per FEU (40ft container) lower than into the US East Coast. This was the case as recently as 31 May when average spot rates were USD 3124 per FEU and USD 4180 per FEU.

However, the steeper declines into the US West Coast since then has seen the spread increase to USD 2015 per FEU.

The spread between average spot rates on these trades will likely return to a more recognisable USD 1000 per FEU once the worst of the trade war volatility passes. But, importantly for shippers, it will likely be due to harder declines into the US East Coast rather than an uplift into the US West Coast.

Ripple effects in South America

If the US tariffs were the rock thrown into the water, we can see the ripple effects spread far beyond the Transpacific fronthauls.

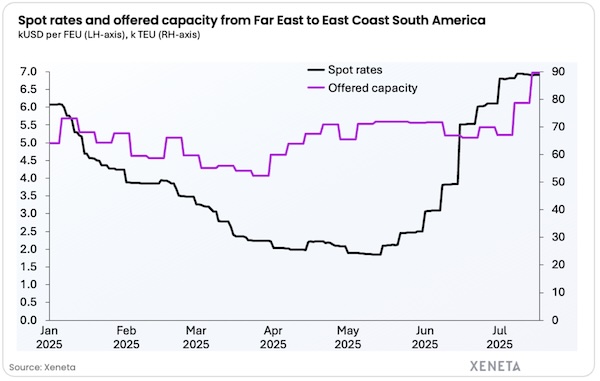

For example, average spot rates from Far East to South America East Coast rose from USD 1 890 per FEU on 1 May to USD 6 945 per FEU on 16 July, an increase of more than 260%.

As carriers rushed capacity back to the US-bound trades following the lowering of tariffs, this came at the expense of the Far East to South America East Coast trade, sending spot rates spiralling.

Further fuel was thrown onto the fire due to demand from the Far East to South America East Coast hitting all-time-record levels in May, just as capacity was being reduced.

Now spot rates are plummeting into the US, carriers are sending capacity back to the South America East Coast to benefit from the higher freight rates. This should bring an end to the spiralling spot rates and is a clear demonstration of the ebb and flow of capacity across the world’s ocean supply chains.

There is an irony that sending capacity back to the South America East Coast to benefit from higher rates will actually put downward pressure on rates, with carriers essentially ruining their own party.

Ripple effects in North Europe

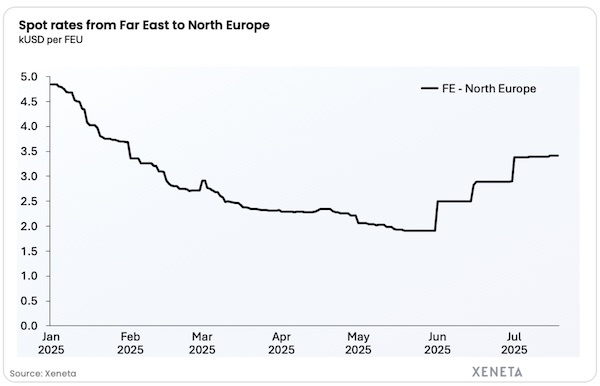

We can also see the tariff ripple effects spread into North Europe, another trade that bucked the global trend of declining spot rates in July.

Average spot rates from Far East to North Europe are up 18% since the end of June and 78% since the end of May to stand at USD 3410 per FEU.

This is driven primarily due to congestion at North European ports, with factors including labor disputes and low water levels in the Rhine causing problems for barges and hinterland transport.

However, we can also trace some of this congestion back to the ripple effects of the tariffs because much of the capacity that was taken from the US-bound trades in the aftermath of “Liberation Day” was also redeployed onto North Europe services.

Timing is often everything, and the resulting record-breaking capacity on these North Europe trades began arriving at ports just as the labor and weather-related disruptions were taking hold.

Where will rates go from here?

You must have sympathy for anyone attempting to set ocean freight budgets for 2026 against this backdrop of volatility.

Shippers must understand the drivers of these rate developments at a global, regional and port level, because, as this blog demonstrates, not all trades will behave in the same way.

The volatility in front haul trades into the US has seen spot rates rise and fall in 2025, but the longer term trajectory is downward. The spike in rates following the lowering of US tariffs was only ever going to be short-lived because shippers cannot frontload forever.

Again, if you are a shipper on the Far East to South America East Coast, the painful spike in freight rates was inevitably going to lose steam as pressure on capacity eased on other major fronthaul trades.

For both US and South America East Coast, rates are only heading downwards for the remainder of 2025 – unless carriers can manage capacity enough to keep rates up or there is another as-yet-unknown market shock (and who would rule that out).

It is a different story for North Europe shippers. The port congestion will stick around for the remainder of 2025, meaning it will put upward pressure on the long term contract market. This a key point of difference with the US-bound Far East front hauls where the long term contract markets have been left relatively unscathed by tariffs and spiking spot rates.

The ripple effect of tariffs will continue to spread and the wider the circles become, the more difficult it will be for shippers to understand their origin and impact.

Index-linked contracts

One way for shippers to ensure supply chain and financial resilience across volatile and unpredictable trades is index-linked contracts, which ensure freight rates remain aligned to market movement.

This prevents long-term agreements being torn up, or regularly renegotiated, in the wake of shocks such as the US tariffs, which, as we have demonstrated in this blog, impact different trades in different ways.

This allows shippers and providers to concentrate on service delivery and supply chain resilience as part of a long-term partnership.

Source: Xeneta